ElmstoneUnion.com Review — Review of a Risky Platform

Introduction

The growth of online investment and banking platforms has created exciting opportunities for many people to access global markets, cryptocurrencies, forex, and commodities. But along with those opportunities comes an increased risk of encountering deceptive operations masquerading as legitimate firms.

One such site that is currently raising concern is ElmstoneUnion.com (sometimes referenced as ElmstoneUnion.com, Elm Stone Union, etc.). While it presents itself as a digital banking and investment firm, multiple red flags suggest that it may not operate as a genuine, regulated institution. This article lays out how the platform appears to work, the patterns of behavior reported by users, and the warning signs investors should identify.

The First Impression: Polished Website, Big Promises

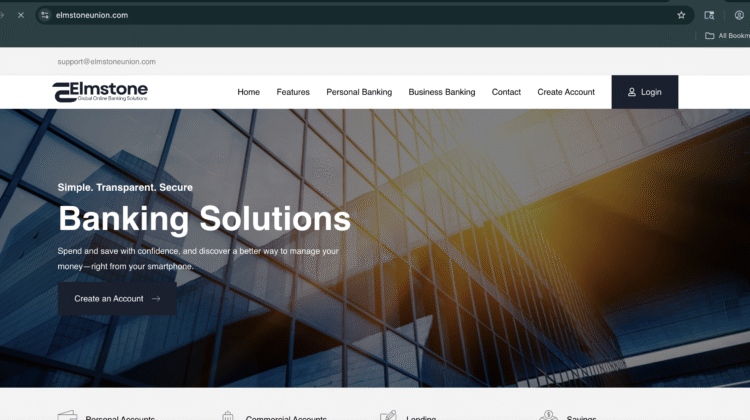

When you arrive at ElmstoneUnion.com, the first impression is one of professionalism and sophistication: slick graphics, a dashboard interface, claims of “instant digital banking,” “investment returns,” “secure trading,” and so on. The layout features what appears to be a bank-style login page, investment portfolios, and perhaps live dashboards (or at least simulated ones). The appearance is designed to instill trust.

The marketing language is compelling: promises of “high yields,” “expert trading,” “crypto integration,” “global banking access from your smartphone,” etc. For someone seeking financial opportunity, these promises can seem attractive.

However, a polished interface and shiny website do not guarantee legitimacy. Many high-risk platforms use professional design specifically to lower users’ guard before harming them.

How ElmstoneUnion.com Appears to Operate

Based on user accounts and analogous platforms, here’s a likely sequence of how ElmstoneUnion.com engages with prospective investors:

1. Entry and Onboarding

A visitor sees an ad (on social media, email, or via referral) promoting ElmstoneUnion.com “bank-investment hybrid” service. The ad claims easy registration and high returns. The visitor fills a registration form with name/email/phone and receives access to a dashboard. Payment/deposit options are presented (often with multiple methods including wire transfer or cryptocurrencies).

2. Personal Contact and Encouragement to Deposit

Shortly after signup, the user gets a call, video chat, or email from someone calling themselves an “account manager” or “investment consultant.” They talk about the user’s goals, emphasize how the platform’s system is advanced, and suggest making an initial deposit (often a modest amount) to test the system. The tone is professional, personalized, and persuasive.

3. “Good Progress” & Upsell

After the initial deposit, the dashboard shows rising balances or gains — sometimes quite significant in a short period. The user may even be encouraged to “withdraw part” of the gain, to build confidence. Then the account manager says: “To unlock full returns / VIP status / algorithmic trading pool, you need to upgrade your account or deposit more.” Urgency may be added: “Offer ends soon,” “limited seats,” etc.

4. Withdrawal Requests & Obstacles

The issue arises when the user asks to pull out larger amounts or their total funds. At this stage, ElmstoneUnion may impose additional conditions: “Please complete verification,” “tax/fee must be paid,” “you must trade X more volume,” or “funds are locked in active trades, wait for settlement.” Communication may slow; customer-support becomes less responsive.

5. Disappearance or Frozen Funds

Eventually, the user may find that withdrawals are denied or ignored, bank wires/crypto transfers cannot be reversed, the website may go offline, the account manager disappears, or the platform rebrands under a new name. The investor may be left with little recourse.

Warning Signals – What to Spot

Here are concrete warning signs that ElmstoneUnion.com or similar platforms may be risky:

-

No verifiable regulatory license: If a financial-banking platform claims to be regulated, the license number should appear in a regulator’s database. Many such platforms provide vague claims without proof.

-

Anonymous ownership or no corporate address: Legit firms have clear company registration details, physical addresses, named directors. Lack of these is a major red flag.

-

Guaranteed or highly-unrealistic returns: Promising large returns with low risk is not consistent with real trading. If the yields sound ‘too good to be true’, they probably are.

-

Unusual payment methods: Crypto transfers or third-party wallets which are irreversible and difficult to trace are common in high-risk operations.

-

High-pressure sales tactics: Urgent calls to deposit more money, “limited-time offers,” or suggesting you’ll miss out constitute manipulative behavior, not professional investment advice.

-

Withdrawal conditions or “unlocking” requirements: When funds are readily deposited but require additional payments, verifications, or fees before withdrawal, it is a very strong warning sign.

-

Lack of independent reviews or credible third-party verification: If you struggle to find objective reviews, or only find user complaints, that suggests caution.

Why These Platforms Thrive

Platforms like ElmstoneUnion.com succeed because they exploit human tendencies and combine that with digital scale and anonymity:

-

Trust via appearance: A professional design gives the illusion of legitimacy, making users feel comfortable depositing funds.

-

Greed and hope: Promises of high returns tap into people’s desire for financial improvement or quick gains.

-

FOMO (fear of missing out): Marketing creates urgency—“opportunity closing,” “limited seats,” etc.—forcing hurried decisions rather than careful ones.

-

Commitment escalation: Once someone deposits some money, they feel invested and are more likely to deposit more. Abandoning the deposit can feel like admitting a mistake.

-

Irreversible fund movements: Use of crypto or untraceable payment routes means once funds leave the user’s control, recovering them is extremely difficult.

These psychological levers make digital finance scams especially effective.

Structural Gaps in ElmstoneUnion.com Operation

From inspection, ElmstoneUnion.com exhibits many structural weaknesses typical of risky operations:

-

Domain age or registration hidden: Sites often register a new domain, hide ownership or quickly rebrand when complaints rise.

-

No clear audit or independent trading records: Genuine investment firms publish third-party audited results or at least credible performance statements. ElmstoneUnion.com does not provide these.

-

Poor transparency around funds custody: Legit brokers explain how client funds are segregated, audited, and protected. Such explanations appear missing or vague.

-

Heavy reliance on individual “account managers”: While many regulated firms assign managers, the difference is in transparency, compliance, and regulation. In risky setups, managers function as pressure-sales agents rather than fiduciary advisors.

The Human Cost

Beyond the technical and financial issues, victims of platforms like ElmstoneUnion.com suffer emotional and psychological damage:

-

Loss of savings: Many invest life savings or large sums believing in the promise of returns.

-

Loss of trust: Once deceived, people often lose faith in legitimate financial services and become more vulnerable going forward.

-

Shame and isolation: Many victims feel ashamed for being tricked and hesitate to speak up, which allows the scam to continue unchallenged.

-

Potential identity exposure: If the platform asks for ID documents or videos, victims may face identity theft or misuse of personal data.

Preventive Habits for Future Investments

While nothing can guarantee safety, adopting these habits significantly reduces risk in the online finance space:

-

Require independent verification: Before depositing, verify the company’s license, read the regulatory registry, and ask for audited performance.

-

Deposit modest amounts first and test withdrawals: Start with minimal funds and attempt withdrawal before increasing.

-

Favor reversible payment methods: Credit cards or regulated payment processors often offer greater protection than irrevocable crypto transfers.

-

Read the fine print: Withdrawal terms, fees, required trade volumes, upgrade obligations—all these should be clear and fair.

-

Ask direct operational questions: Who holds the funds? What bank or custodian is used? What risk disclosures are provided? Legit firms answer transparently.

-

Use trusted personal advisers or colleagues: Especially if an “advisor” from the platform is urging large deposits quickly.

End Note

ElmstoneUnion.com casts itself as a modern fintech or banking-investment hybrid platform—but the signs suggest it may instead operate as a high-risk or fraudulent scheme. From professional design and persuasive sales tactics to unverifiable credentials and withdrawal obstacles, the platform ticks many of the boxes for investor caution.

This review does not assert definitively that ElmstoneUnion.com is a scam (that requires regulatory adjudication). Instead, it presents the consistent patterns and warning signals that serious investors should treat as red flags. If you’re considering depositing funds with ElmstoneUnion.com or a similar platform, proceed only after full verification, start with minimal funds, test withdrawal capability, and maintain a healthy level of skepticism.

In digital finance—while opportunity is abundant—prudence and verification remain essential. Trust should never be given solely based on appearance or promise.

Conclusion: Report ElmstoneUnion.com Scam to AZCANELIMITED.COM?

Based on all available data and warning signs, ElmstoneUnion.com raises multiple red flags that strongly suggest it may be a scam. From its unregulated status to its anonymous ownership and unrealistic promises, this platform lacks the transparency and trustworthiness expected from a legitimate financial service provider.

REPORT THIS PLATFORM TO AZCANELIMITED.COM

If you’re thinking of investing through ElmstoneUnion.com , extreme caution is advised.